Adrienne Hines is a bankruptcy attorney who has helped people get out of debt for nearly three decades and has read the “stop buying lattes” crowd so you do not have to. A lot of that advice comes from people who never faced shutoff notices or collection calls.

If you are tired of guilt and one-size fixes, this video points to titles that meet you where you are. We focus on tools that reduce shame, explain the system, and give you practical next steps. Watch the video, or keep reading for the FAQs.

Frequently Asked Questions

- Why do so many financial literacy books miss the mark for real people?

- What should I look for in a financial book if I am in debt?

- Is “stop buying lattes” useful advice?

- Should I avoid bankruptcy at all costs?

- Which book helps me set up a simple money system that works?

- Which book explains why I make money mistakes even when I know better?

- Why would a bankruptcy book belong on a financial literacy list?

- Can I build wealth while I am still drowning in debt?

- How do I pick a book that fits my reality, not someone else’s?

- Where can I talk to someone for free about my debt?

FAQ: Why do so many financial literacy books miss the mark for real people?

They miss because many authors wrote from comfort, not crisis, and their advice does not match today’s costs or collection pressure. Tips like skipping small purchases ignore rent, medical bills, and interest that outruns minimum payments. Books that fail to acknowledge fear, unopened mail, and legal relief tools end up shaming readers instead of helping them.

FAQ: What should I look for in a financial book if I am in debt?

Look for books that speak directly to your situation, explain credit reporting in plain language, and give steps you can start immediately. The right book respects legal options like bankruptcy and focuses on systems, not guilt. Prioritize authors who work with real people and provide scripts, checklists, and realistic paths forward.

FAQ: Is “stop buying lattes” useful advice?

No. Small spending cuts do not fix a crisis driven by high interest, fees, or income gaps. Skipping coffee will not solve impossible math. Focus on big levers like automation, lowering interest, correcting credit errors, and using legal protections when needed.

FAQ: Should I avoid bankruptcy at all costs?

No. Bankruptcy is a legal tool, not a moral failure. For many people, it is the fastest way to stop collection pressure and reset. When debt stalls progress every month, relief must come before rebuilding.

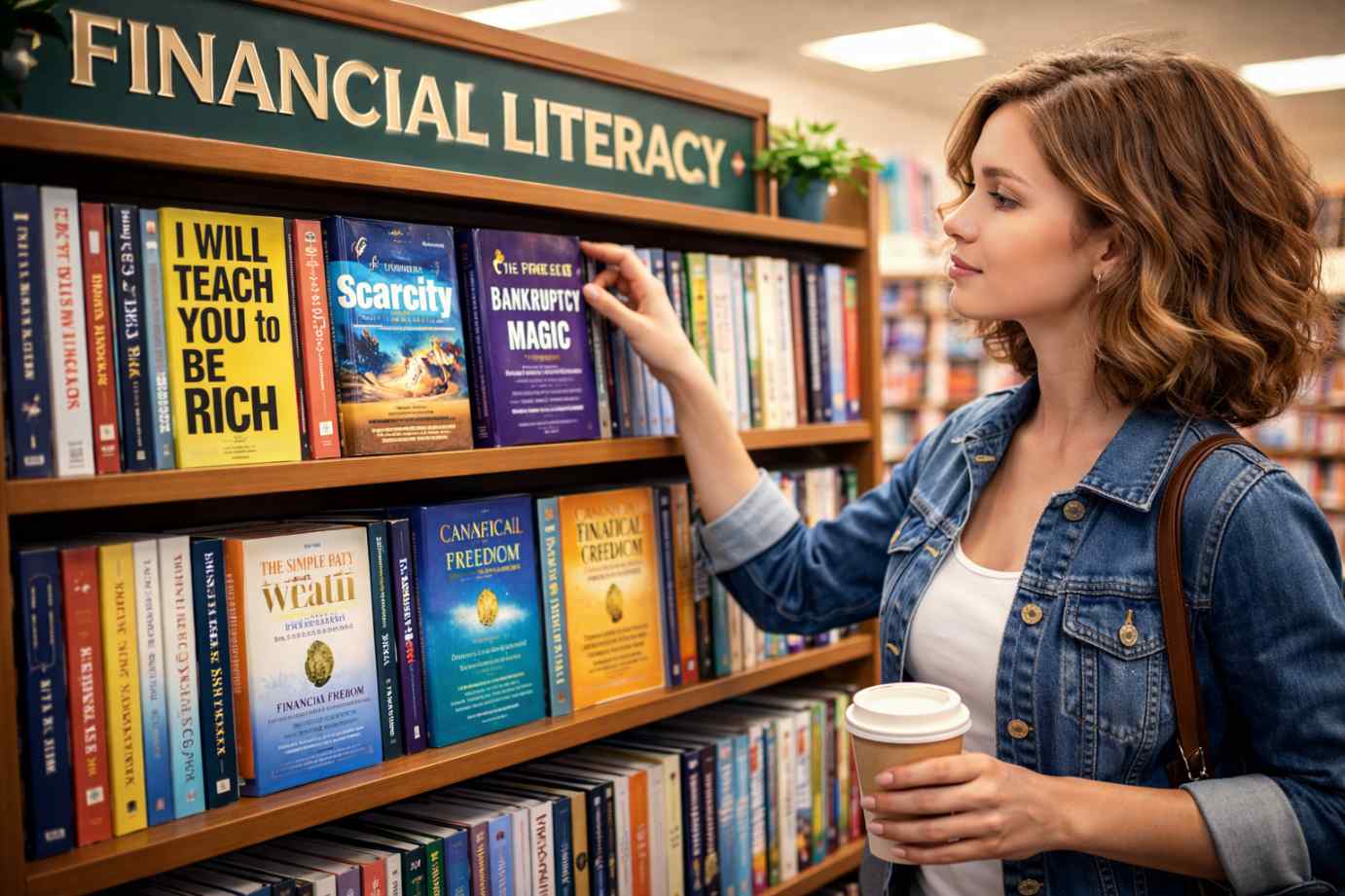

FAQ: Which book helps me set up a simple money system that works?

I Will Teach You To Be Rich by Ramit Sethi focuses on automation, guilt-free spending, and practical systems that run even on busy weeks. It emphasizes action over perfection and gives readers rails they can follow without shame.

FAQ: Which book explains why I make money mistakes even when I know better?

Scarcity by Mullainathan and Shafir explains how lack of time, money, or energy narrows thinking and leads to panic decisions. Understanding this mental load reduces self-blame and helps you design guardrails that prevent repeat mistakes.

FAQ: Why would a bankruptcy book belong on a financial literacy list?

Because many people need a clean break before any money plan can work. Bankruptcy Magic by Adrienne Hines explains debt relief with dignity and clarity. It turns a frightening topic into an understandable, honorable path forward.

FAQ: Can I build wealth while I am still drowning in debt?

No. High-interest debt blocks saving and investing. Wealth building begins only after the pressure is reduced. Relief creates the space where systems and habits can finally stick.

FAQ: How do I pick a book that fits my reality, not someone else’s?

Choose books that sound human and reflect your exact pain points, like collections, credit errors, or bill negotiations. Skim a chapter that matches your situation. If it gives steps you can take today, it is likely a good fit.

FAQ: Where can I talk to someone for free about my debt?

Use the link in the video description to speak with a debt professional at no cost. A short conversation can help you sort options, decide what to read, and choose the right next step.

Disclaimer: This article is for general educational purposes only and does not constitute legal or financial advice. Bankruptcy laws and debt collection rules vary by state. If you’re dealing with debt collection or considering bankruptcy, you should speak with a licensed bankruptcy attorney who can review your specific situation.